- cross-posted to:

- comicstrips@lemmy.world

- cross-posted to:

- comicstrips@lemmy.world

You must log in or register to comment.

pan to tax preparation companies taking turns sucking off Uncle Sam

My son made a mistake on his state taxes and his return was rejected. The letter he got back basically said “we couldn’t verify your reported property taxes, so you can resubmit a correction or do nothing and accept our version of your taxes” (where he gets back about $200 less because of a typo.)

So, like, yeah. They’re just comparing your notes to theirs, with the default benefiting the state.

Seems like the property taxes would be the easiest thing in the world for them to verify. Unless they’ve been lying to themselves.

There’s a lot. Every tax form you get is submitted to the government as well. W2,1095 a, 1099, property taxes etc. For most people, the government could just send a letter saying: we have all the documents. Do you want to itemize or take a standard deduction? Do you have anything else to report? Cool. The people that would still have complicated taxes would be the self employed.

Yes, it would be helpful if people didn’t have to chase down a bunch of forms that were submitted to the IRS already. But for instance in our family there’s a lot of medical expenses, well over the minimum for us to deduct them, so we’d still want to do that.

Yeah itemized deductions would still need to be offered, but for many people the work would be minimal since it usually makes sense to select the standard deduction. That’s horrible that you even have to pay that much for medical expenses but that’s a whole other conversation lol.

I believe they had a typo entering their PIN. The property number is like 15 digits long with multiple hyphens. It was fine last year, but this year they got “wE cAn’T vErIfY yOuR pRoPeRtY tAxeS” .🙄

No panning required, just zoom out on the last frame and its quite explicit, with Unc’s thought bubble being “I’M HAVING ONE!”

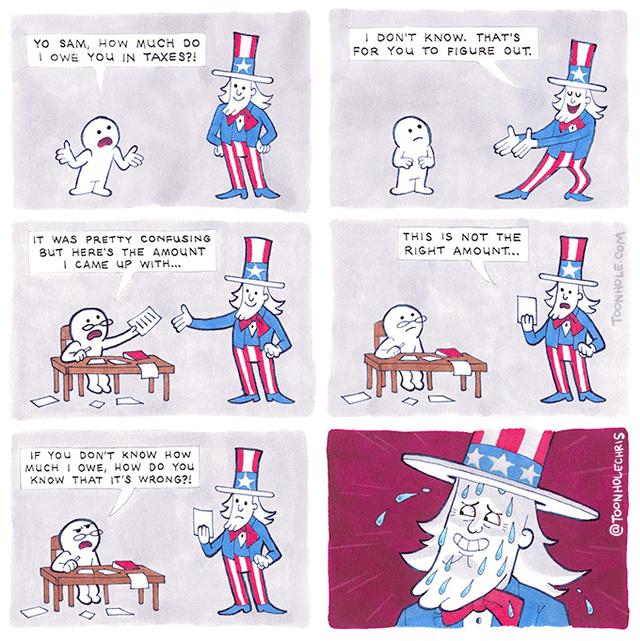

They don’t actually know. If they think something looks suspicious, they do an audit, and then they know.

The vast majority of people’s taxes fillings are taken on good faith.

I got audited a few years back. I claimed something that set off a red flag–deducted tuition for a grad program as a business expense.

I freaked out at first because I thought I must have messed something up or that they knew I messed something up.

What I discovered is that: at the end of the day these folks are probably just as annoyed as you that they got another “audit” in their pile. And being flagged doesn’t mean you are wrong. It means they need more information before they can decide.

I wrote a detailed response with the actual flow chart from their own guidance, I circled the decisions on the chart, and then provided proof of each decision in my letter. Basically I held their hand and showed them I could legit deduct it.

They were like “oh, cool thanks! You’re good. Actually, you could have itemized x if you have receipts for it and you’d get a bigg r deduction if you wanted to amend”

That’s when I realized they don’t really check everyone’s taxes at all. They have a system that flags certain situations for further review. I guess, in my case, people lie or mess up this tuition deduction a lot so they double check.

Mind you, if you routinely fudge your taxes, they will eventually notice something strange, or hit you with a randomized audit. Then, whoops, we found something! Better take a closer look at all your past filings too…

They don’t actually know the final amount, but they do have an independent expectation for certain items.

If your job withholds income tax then it is paid quarterly to the government, so they know how much you made and how much taxes you should be paying.

If you win a large sum of money in the stock market or gambling at a casino then the broker or management company reports a tax bill to the IRS. The same happens for large early withdrawals of retirement funds.

They also know information based on previous returns, like how many kids you have or if you own a home.

They may not know it down to the dollar amount you’ll be paying because of the complexity of the US tax code and the deductions you’ll claim. For example, the government has no record of you purchasing a $600 electric car charger but you can claim that on your taxes to reduce your tax liability. That being said, if you under-report the amount you made at your job they will almost surely audit you if the number reported by your employer doesn’t match the number you provide.

In many countries, the government does have a record of you purchasing that electric car charger as long as you ask the seller to include your tax number in the receipt - which you need to do if you want to file it - and it all comes automatically pre-filled in my tax deductions. Its become really easy to do taxes, it’s literally 3 clicks for most people.

That almost sounds sane

“Listen bub, I’m just telling you what Intuit and H&R block pays me to tell you. So yeah, I both know and don’t know what you owe. Let’s call it Schrodinger’s taxes and call it a day.”

You don’t know what we know about what you owe.

The answer of course is that the IRS doesn’t know how much you owe, and it isn’t feasible for them for figure out exact numbers for everyone with the tax code as complicated as it is. So, they audit a fraction of Americans every year to keep everyone honest. It’s a bad system that taxes are so complicated but it’s not a conspiracy.

It absolutely is a conspiracy though:

Except the federal government literally this year started instituting a free, public filling service to get around TurboTax. And they fought it tooth and nail.

There is a conspiracy, but it’s not a federal government conspiracy. It’s just a bad system that certain companies conspired to take advantage of.

I mean, the tax system is so bad because tax preparers like Intuit bribe politicians to keep it that way.

It is engineered the way that it is to provide loopholes for rich people.

God, I would hate to have to work out my taxes every year laughs in British

Hey, some of us do have to do taxes, but you pretty much follow a questionnaire on the gov.uk website then fill out some numbers from paperwork you’ll already have (P60, payslips, etc). I had to whip out the calculator once to add up 12 numbers for my student loan.

Could probably do it in under an hour if you’re not doing anything unusual.

The American system sounds very much not that.

For many Americans it’s actually pretty simple as long as they’re working with a standard W-2 (form you get from your employer with the year’s wages and taxes and stuff filled out). Many tax prep services will even import these numbers automatically and all you have to do is click through the questions and optional things like if you want to donate your returns to anything or pay estimated taxes for the next year - mostly stuff that most people aren’t concerned with anyway.

Taxes here start getting complicated when you are an independent contractor (you’re responsible for holding out taxes from your income since you don’t have an employer to do it for you) and/or have non-standard sources of income like stocks, shares, real estate holdings, etc. which the IRS may or may not have information on, thus why you need to provide the info.

Most of what has made calculating taxes and paying/getting returns a pain in the ass is tax prep companies like TurboTax lobbying to make and keep the tax filing process a confusing one, with the goal of steering you into paying for the non-free filing options.

I was shocked how easy it was to do my taxes when I was poor (back before the online services even). Just went to the library and spent half an hour filling out a 1040EZ form and dropping it in a mailbox.

It’s harder now that I actually have contributions to retirement, back when I owned a house, make considerably more, have two kids and a wife that’s going to school, etc. But still took me less than an hour.

And I would argue that if it takes you more than an hour to do taxes, you both should and can afford someone to do taxes for you.

Oh interesting yeah, so doesn’t actually sound too complex for most people then.

I’m a little confused about the last part, what are the main differences between paid and free services if it’s as simple as you describe with the W-2 form?

The legal requirement for tax prep services like turbo tax to offer free filling is, in true capitalist style, a qualified one. All they’re really required to offer for free is the basic tax return form - Form 1040. Even with a typical W-2 job, you may have additional non-standard forms to fill out, particularly relating to healthcare coverage since here in America, of course that’s tied to your employment.

When you start getting those non-standard forms, tax prep services can start charging you to upgrade to the premium tier that handles those forms for you - your alternative being to file online what you can for free and doing the rest by hand, but being non-standard forms they of course read like stereo instructions so good luck with that.

At first it doesn’t seem that bad - you sigh and say, “Fine, it’s only $32.” But then you get to the last page and find out it’s $32 for each return filed - most Americans file at least 2, federal and state. So now it’s $64. And say you’re in my situation where you live in a city that straddles a state line - many here work in one state but live in another, so that a federal and two state returns. Now we’re up to $96. You want your returns direct deposited to your bank instead of a paper check? Another fee, because fuck trees. So by the time it’s over you’re paying over $100 in essentially convenience fees for the very companies that make tax prep miserable to do it all for you. To make you feel better about it the services will say you’re also getting stuff like audit protection and various other fluff, nothing that really costs them anything to provide.

stuff like audit protection

“Who’s doing the audit?”

“You wouldn’t believe it”

Yea most of those services are a sham. I use freetaxusa I think it was like 23 bucks to file my state ones and the fed ones are free. They seem to have all the stuff you need for more complicated filings but I have the basic bare minimum.

I used CashApp’s new tax service to file this year. Federal and State were free, took all but a few minutes to complete. Being a new service, they still have filing situations that aren’t covered though - for example, the non-resident status that I mentioned above where you work and live in different states.

The actually free services are out there, they just don’t have the advertising budgets that TurboTax and H&R Block have.

Even then buying and selling stocks, having a 401k, IRA, etc. doesn’t even make it complicated. You just have to fill out a 1099-B/DIV/INT and then list your contributions to your retirement accounts.

I don’t know why people pretend it’s so hard. You spend 30 minutes every year answering a few questions and punching numbers into boxes from a few documents that are sent to you by your broker/bank/employer. It’s also only $15 at FreeTaxUSA.

Opening the accounts you report to the IRS is arguably more difficult than filing them on your taxes.

The main point I think is that American taxes aren’t typically difficult, but rather inconvenient - by design of the tax prep companies lobbying to keep it that way.

You guys have to fill in numbers? The Australian Tax Office pre-fills your tax return with the data they get from your bank and employer, so most people can do it in 5 minutes by clicking next a bunch of times.

To be fair the vast majority have it fully automated PAYE and don’t even have to file. Though it’s a good point, I’m pretty sure the tax forms you get the numbers from are a standard format, I wonder why they haven’t got something like that in place here.

At the very least you should be able to upload the PDFs from your work payroll as the end of year forms and it could pull the details from those

Um, The American system is exactly like that.

Apparently so! I’m just finding this out

I had got the impression that it was some laborious task where you basically had to hire an accountant or pay for some software

Its a nice break from figuring out if the amount my medical providers charged me lines up with the estimation of benefits provided by my medical insurance company and trying to get a denied claim paid.

I know what you mean. Laughs in Dutch

because they won’t tell you about the loop holes and exceptions you could be taking advantage of.

yep. They won’t tell us if we payed them too much, they’ll only tell us if we didn’t pay them enough 😡

A few years back in Massachusetts actually, the taxpayers hit an annual threshold cap and the state had to refund some of the money to those who filed.

works as well with just the last two panels

Wow, yeah – way punchier

This year I think the IRS is rolling our free preparation (federal, some states offer it to I think).

Go check it out.

But yeah this could all be automated. Just another cigarette in your eye for daring to exist in the conservative fascist multiverse.

I looked into this. I didn’t qualify due to having an HSA.

Yeah this year it seems there’s a lot of restrictions. I’m hoping next year it will be accessible to more people

They are! I qualified for free federal and state - admittedly, I have very simple taxes - and it was easy and fast. Even got my refund in under the estimated time!

I hate fucking taxes. Just stayed on a call with Fidelity because I overpaid my 401k by a few dollars and they don’t know how to set a reimbursement. Now I’m on a call with Anthem because they don’t know why I never got my 1099-SA. Fuck. I really fucking hate taxes.

Of course they have to mail it to me. Now I gotta figure out how to calculate my own 1099 SA.

Just file for an extension, it’ll give you until October (?) to complete your taxes with the proper paperwork.

Few years ago, I estimated my pay/taxes because a former employer never mailed me my W2 since they just sucked. I’m foggy on all of the specifics, but I remember getting a letter saying they couldn’t verify the info from that W2, and that I wouldn’t get my refund until it was verified.

Got the company to send me my actual W2, filed a revised return, and ended up owning like $1700, even though it had told me before the letter I’d get a refund of like $3k. Annoying as fuck, but ultimately my fault, I should’ve just waited for the W2 and filed for an extension in the meantime.

Following year, I got a letter from the IRS saying they owed me $1300 that was never released due to my tax shenanigans the previous year.

Moral of the story: just file for the extension, save yourself the anxiety and headache.

I just ended up using ChatGPT and manually calculated the 1099 SA using statements that were available.

I owe like 11k so if I file an extension, I will have to pay interest.

I enter in my w4 and take the standard deduction. Takes me 5 minutes.

Haven’t owed since I had a retail job that reset my withholding when I got promoted to make it look like I got a bigger raise.

Do you not earn interest on any accounts? No loans on which you pay interest? Are you a student?

Like I said: standard deduction. Those numbers never come close to make itemized deductions worth the time and effort.

Interest is income, so your W-2 won’t be enough to account for that. You’ll also need to go to any banks, taxable brokerage accounts, etc, because that money will impact your taxable income. Still not a ton of work, but it’s still more than just W-2 + standard deduction.

Thanks for the casual assumption brokerage accounts enter into the picture.

No savings for interest, all income goes to debts and expenses.

But I am doing relatively great almost entirely because my housing costs are comparatively low and locked in for 27 more years.

That’s fair. My point though is that with higher IRS funding, poorer people are probably going to get audited more, and if you’re only using your W-2, you’re probably missing something and could get caught with an audit.

Other things that could factor in:

- bank account bonuses - i.e. that $100 to sign up for an account or whatever (usually doesn’t include credit card rewards, but that can also depend)

- gambling wins

- interest on inheritance money, if any

Most people aren’t going to have anywhere near enough taxable investment income for that to matter.

I think I got about $.87 in interest payments from bank accounts in the past year. I don’t think that’s going to make a huge difference in taxable income.

You need a better bank account then.

Let’s say you have $10k in cash (typical emergency fund) and get 4% on it (relatively competitiv; e.g. Ally gives 4.25%), that’s $400 in interest (not including compounding), which is a reportable amount of income. If you’re doing something clever or have a bit more cash for some reason (e.g. saving for a house), you could easily get into more interesting amounts of money.

$10k in cash (typical emergency fund)

There’s your mistake right there, thinking people have even $10k to serve as a spare emergency fund.

I don’t even have a thousand spare right now for an emergency.

It’s just an example. You can get semi-interesting numbers with just regular cash flow, depending on what kind of interest your accounts get. Let’s say you make $60k/year and your money sits in your account on average for 5 days. So that’s essentially the same as $800-900 (

($60k / 26) * (5/14)) earning whatever your interest rate is on your account. That’s something like $20-40 for 2-5%. That money counts.Your risk of an audit increases the more discrepancy the automated checks find. This article claims poorer people are getting targeted more and more, so I think it makes sense to take a few extra minutes to report all of the little accounts you may have.

I had like $6k savings until I did my taxes and apparently everything I saved up was how much I owed the tax man. I thought I had actually gotten ahead but turns out that was an illusion lol

Yea I appreciate the dude trying to make sure people don’t forget stuff and get fucked by the irs but he’s a bit privileged thinking we’re all as well off as he is.

What is special about today?

Last day to file taxes in the US without having filed for an extension.

He only knows because your employer ratted you out

Your employer doesn’t know all your sources of income if you have independent stuff going on.

If you have taxes witheld the will know. Only way to avoid that is through contract labor cash only

What? No. They only know the amount you asked them to withhold, and that could get you in trouble if you specify dependents then tell everyone you don’t have any or something. Also if someone is living in your house, making less than 4700 for the entire year, they can be claimed as a dependent, which means you don’t even have to have kids. How would your work even know?

W4

Most of that stuff is pretty optional, and that’s for automatic withholding info. You can correct this all on your tax return. This form is more for you to have convenience during return time, and it even says you can exempt yourself from the form for multiple conditions. I don’t see why you need to get paid in cash still, like your original comment.

Already completed my taxes and been refunded. Even jad to pay $100 is penalties for not paying the total of 2022s bill. So i’m done til next year

Ok but what about this… W5. Checkmate.

What is that? A state tax form?

deleted by creator

I mean, that’s essentially what our taxes are. Things vary based on tax brackets, state, dependents/spouses, and total earnings of course, but we all have a base tax.

The hard part of taxes is usually deductions, or when you start having things like investments or small businesses.

I guess that was some sort of short-circuit on my part?

No, you’re right that it’s extremely complicated. But the complexity doesn’t come from the base rates. You’re likely thinking of the process as a whole instead of the starting point.

{kind=link}