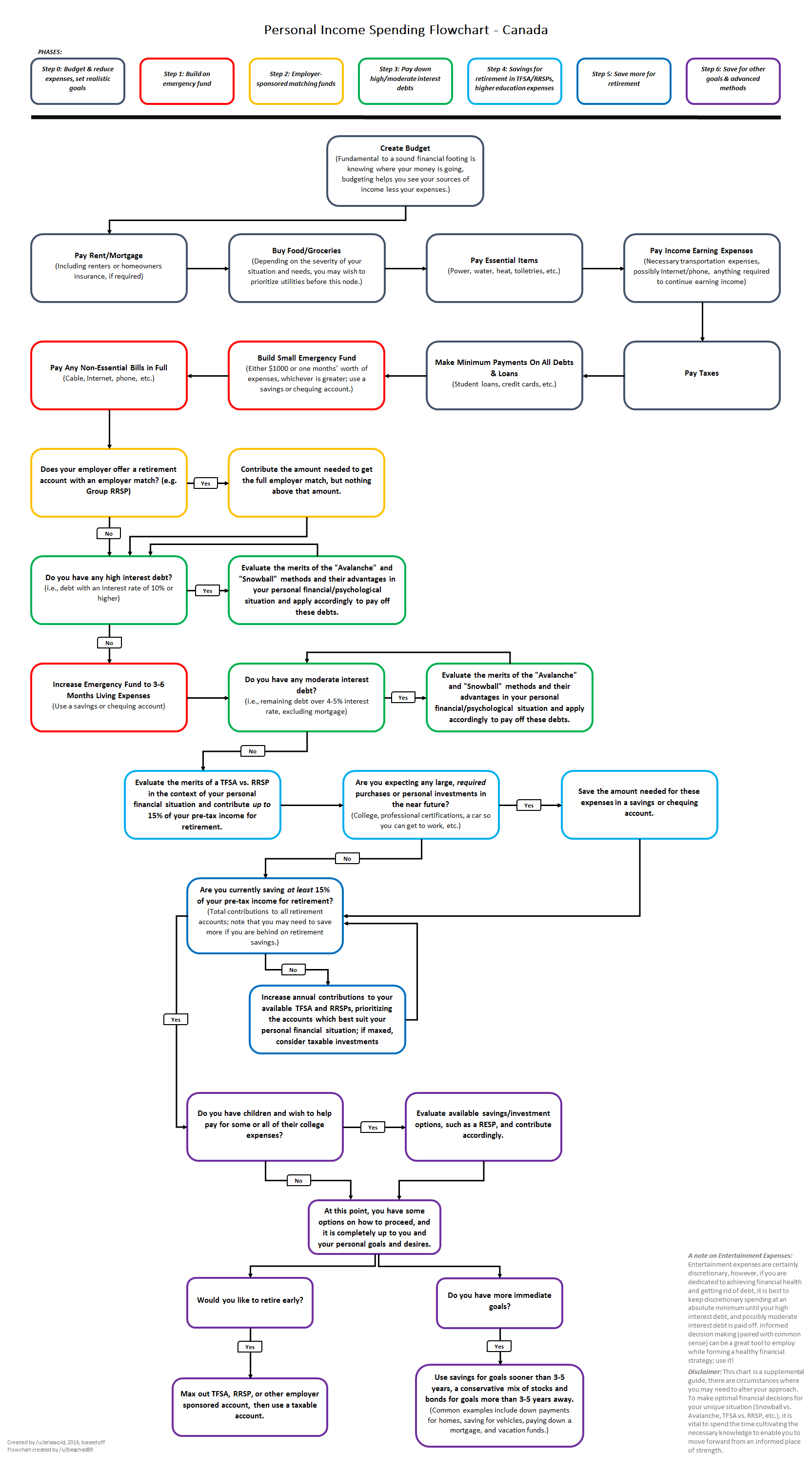

I’m surprised that paying off high interest debt is so low on the flow chart. I personally don’t know if it’s a good idea to follow this chart as it is.

Interesting take: how would you put it higher? IMO, almost all the previous steps (except the one about employer match) are related to living expenses, which are in my opinion more important than something that can be cleared through bankruptcy, so I don’t see how that could move much higher.

I’d put it above a small emergency fund, which you need precisely to avoid bad debt. It hardly makes sense to set aside $1000 when you have $1000 in CC debt. I’d also put it above non-essential bills. That list is weird because I would consider cell phone and internet absolutely essential. But if it’s truly non-essential, like cable or a game subscription, I would cancel until I don’t have bad debt.

The employer match is actually maybe the only one I might keep, since you get an instant 100% ROI.

{kind=link}

I’m surprised that paying off high interest debt is so low on the flow chart. I personally don’t know if it’s a good idea to follow this chart as it is.

Interesting take: how would you put it higher? IMO, almost all the previous steps (except the one about employer match) are related to living expenses, which are in my opinion more important than something that can be cleared through bankruptcy, so I don’t see how that could move much higher.

I’d put it above a small emergency fund, which you need precisely to avoid bad debt. It hardly makes sense to set aside $1000 when you have $1000 in CC debt. I’d also put it above non-essential bills. That list is weird because I would consider cell phone and internet absolutely essential. But if it’s truly non-essential, like cable or a game subscription, I would cancel until I don’t have bad debt.

The employer match is actually maybe the only one I might keep, since you get an instant 100% ROI.